Introduction

Under India’s GST regime, the concept of supply forms the foundation of taxability. Among the most misunderstood and litigated aspects of supply are Composite Supply and Mixed Supply. Though they may appear similar, incorrect classification can result in wrong tax rates, denial of input tax credit (ITC), interest, penalties, and prolonged disputes with tax authorities.

With digitised compliance systems, advance rulings, and increased departmental scrutiny, accurate classification has become critical. This article explains the distinction between Composite and Mixed Supply under GST through practical case studies and professional guidance.

Concept of Supply under GST

Section 7 of the CGST Act defines supply to include all forms of supply of goods or services made for consideration in the course or furtherance of business. GST liability depends not only on whether a transaction qualifies as a supply, but also on how that supply is classified.

When multiple goods or services are supplied together for a single price, determining whether the transaction is a Composite Supply or a Mixed Supply becomes essential for applying the correct GST rate.

Composite Supply – Meaning and Practical Application

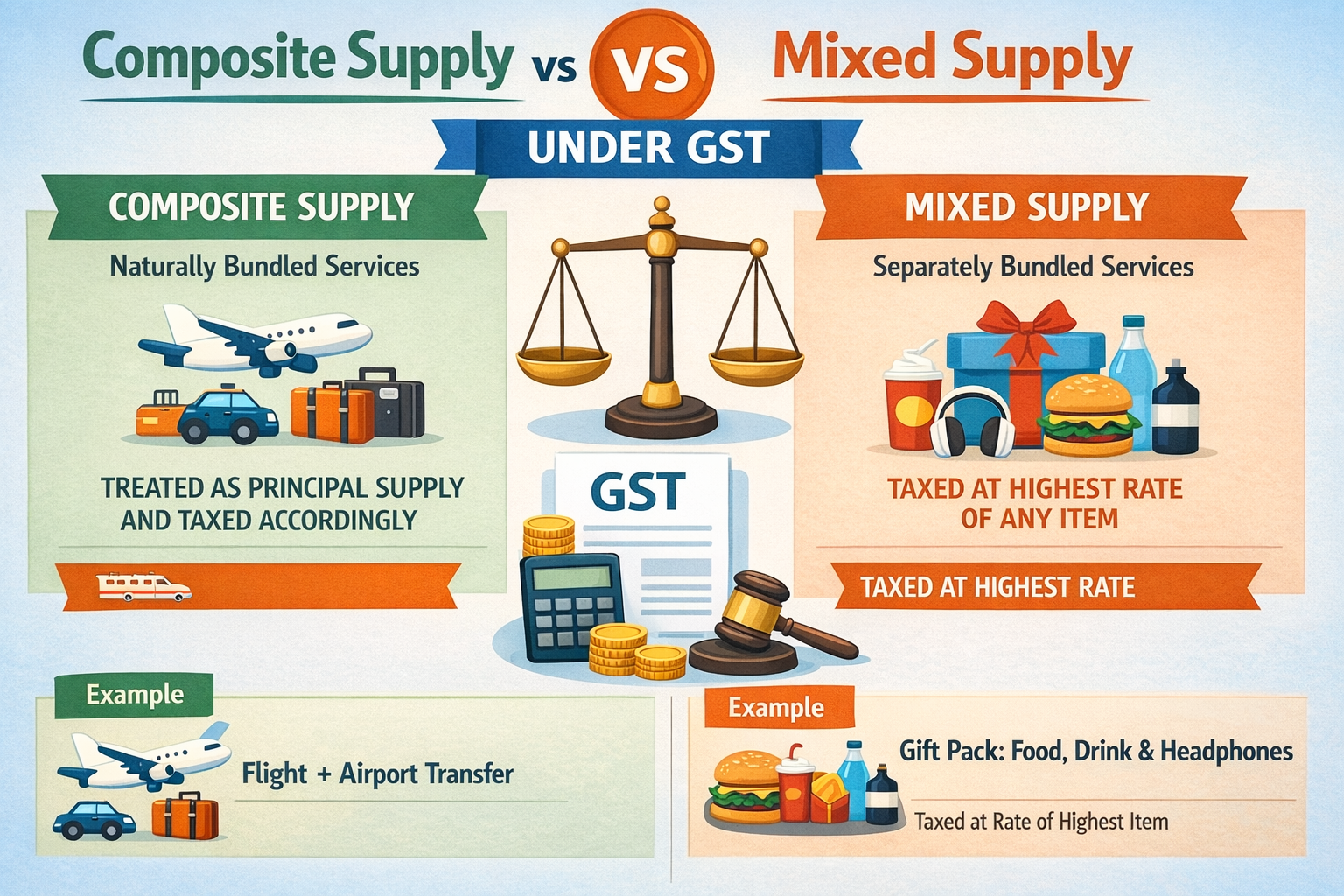

Section 2(30) of the CGST Act defines Composite Supply as a supply consisting of two or more taxable supplies that are naturally bundled and supplied together in the ordinary course of business, with one supply identified as the principal supply.

In a composite supply, the GST rate applicable to the principal supply applies to the entire transaction. The other supplies are ancillary and do not determine the tax treatment.

A common example is hotel accommodation with breakfast, where room rent is the principal supply and breakfast is incidental. Similarly, software supplied along with installation or customization services is treated as a composite supply, with software being the dominant element.

Case Illustration:

An ERP software company supplies software along with mandatory customization services. Although both elements are taxable at 18%, the customer’s primary intention is to purchase the software. Customization merely enables effective use of the software. Accordingly, the transaction qualifies as a composite supply, taxable at 18% on the entire value.

Mixed Supply – Meaning and Practical Application

Section 2(74) of the CGST Act defines Mixed Supply as two or more individual supplies of goods or services made together for a single price, which are not naturally bundled and can be supplied independently.

In mixed supply, there is no principal supply. The entire transaction is taxed at the GST rate applicable to the highest-taxed component in the bundle.

Mixed supplies are commonly seen in promotional offers, festive gift hampers, and combo packs, where products are bundled for marketing convenience rather than business necessity.

Case Illustration:

A Diwali gift hamper contains chocolates and wine sold at a single price. Since both items can be sold independently and are not naturally bundled, the transaction qualifies as a mixed supply. As wine attracts a higher GST rate, the entire hamper is taxed at that rate.

Key Practical Case Studies

Works Contract:

A contractor supplies construction services along with materials. Under GST, works contracts are treated as composite supplies, with works contract service being the principal supply. GST is levied on the entire contract value at the applicable rate.

Hotel and Tourism Package:

A hotel offers a package including accommodation, breakfast, and sightseeing. Since accommodation is the primary element and other services are ancillary, the transaction qualifies as a composite supply, taxable at the rate applicable to hotel accommodation.

E-commerce Electronics Bundle:

An online seller offers a laptop, mouse, and software as a discounted bundle. Each item can be sold separately and none dominates the transaction. This constitutes a mixed supply, taxable at the highest GST rate applicable among the bundled items.

Professional Challenges and Risk Areas

The biggest challenge lies in identifying the principal supply, which requires analysing business intent, customer perception, and market practice—not merely contract wording. Promotional bundling often leads to mixed supply classification, increasing tax liability.

Tax authorities and courts consistently apply the principle of substance over form. Advance rulings such as Infosys Technologies (Composite Supply) and ITC Ltd. (Mixed Supply) highlight the importance of factual evaluation.

Practical Compliance Guidance

Businesses should carefully evaluate bundled transactions by identifying all components, determining whether supplies are naturally bundled, and assessing whether one supply dominates. Proper documentation in contracts and invoices is essential to defend classification during audits and assessments.

A simple rule of thumb is:

- If supplies are naturally bundled with a dominant element, it is likely a composite supply.

- If supplies are independent and bundled for convenience, it is likely a mixed supply.

Conclusion

The distinction between Composite Supply and Mixed Supply under GST has significant tax implications. Composite supplies are taxed at the rate applicable to the principal supply, while mixed supplies attract the highest GST rate among their components.

Careful analysis, consistent business practices, and proper documentation are essential to avoid disputes and ensure compliance. Under GST, correct classification is not merely technical—it is a critical element of effective tax risk management.